With the Bank of Japan trying yield curve control, negative GDP growth in the United States and cracks showing in the eurozone, bitcoin looks like a smart bet.

Watch This Episode On YouTube or Rumble

Listen To This Episode Here:

“Fed Watch” is the macro podcast for Bitcoiners. Each episode we discuss current events in macro from across the globe, with an emphasis on central banks and currencies.

In this episode, Christian Keroles and I cover developments in Japan, in regards to yield curve control (YCC); in the U.S., in regards to growth and inflation forecasts; and in Europe, in regards to the concern about fragmentation. At the end of the episode, we celebrate the 100th episode of “Fed Watch” by reviewing some of the guests and calls we have made throughout the show’s history.

Big Trouble In Japan

The economic troubles in Japan are legendary at this point. They have suffered through several lost decades of low growth and low inflation, addressed by the best monetary policy tools of the day, by some of the best experts in economics (maybe that was the mistake). None of it has worked, but let’s take a minute to review how we got here.

Japan entered their recession/depression in 1991 after their giant asset bubble burst. Since that time, Japanese economic growth has been averaging roughly 1% per year, with low unemployment and very low dynamism. It’s not negative gross domestic product (GDP) growth, but it’s the bare minimum to have an economic pulse.

To address these issues, Japan became the first major central bank to launch quantitative easing (QE) in 2001. This is where the central bank, Bank of Japan (BOJ), would buy government securities from the banks in an attempt to correct any balance sheet problems, clearing the way for those banks to lend (aka print money).

That first attempt at QE failed miserably, and in fact, caused growth to fall from 1.1% to 1%. The Japanese were convinced by Western economists, like Paul Krugman, who claimed the BOJ failed because they had not “credibly promise[d] to be irresponsible.” They must change the inflation/growth expectations of the people by shocking them into inflationary worry.

Round two of monetary policy in 2013 was dubbed “QQE” (quantitative and qualitative easing). In this strategy, the BOJ would cause “shock and awe” at their profligacy, buying not only government securities, but other assets like exchange-traded funds (ETFs) on the Tokyo Stock Exchange. Of course, this failed, too.

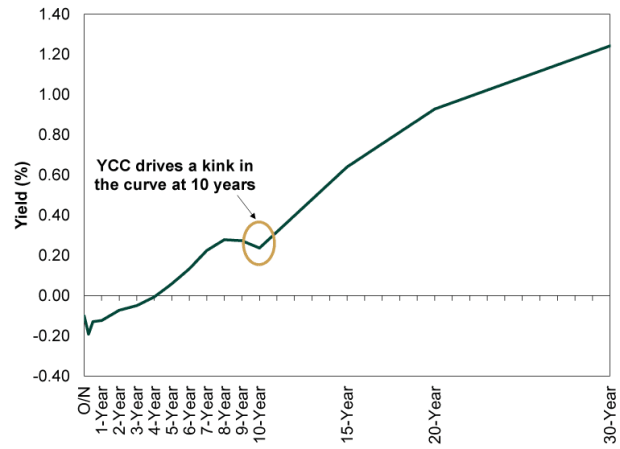

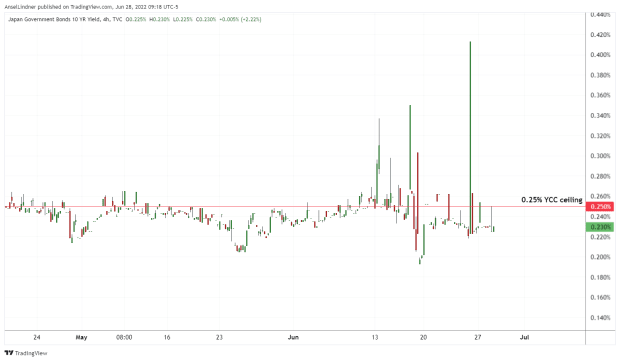

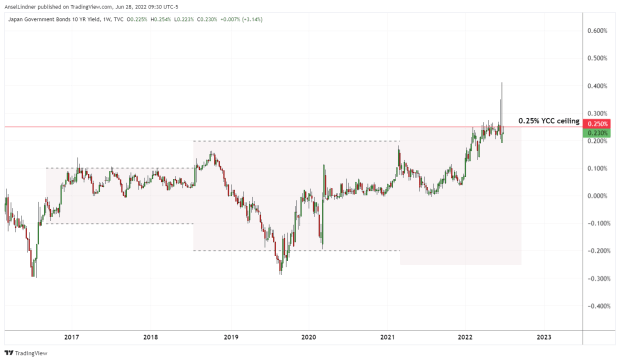

Round three was the addition of YCC in 2016, where the BOJ would peg the yield on the 10-year Japanese Government Bond (JGB) to a range of plus or minus 10 basis points. In 2018, that range was expanded to plus or minus 20 basis points, and in 2021 to plus or minus 25 basis points, where we are today.

The YCC Fight

As the world is now dealing with massive price increases due to an economic hurricane, the government bond yield curve in Japan is pressing upward, testing the BOJ’s resolve. As of now, the ceiling has been breached several times, but it hasn’t completely burst through.

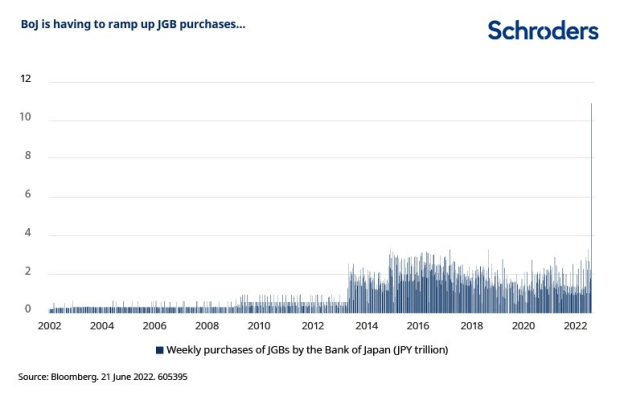

The BOJ now owns more than 50% of all government bonds, on top of their huge share of ETFs on their stock exchange. At this rate, the entire Japanese economy will soon be owned by the BOJ.

The yen is also crashing against the U.S. dollar. Below is the exchange rate for how many yen to a U.S. dollar.

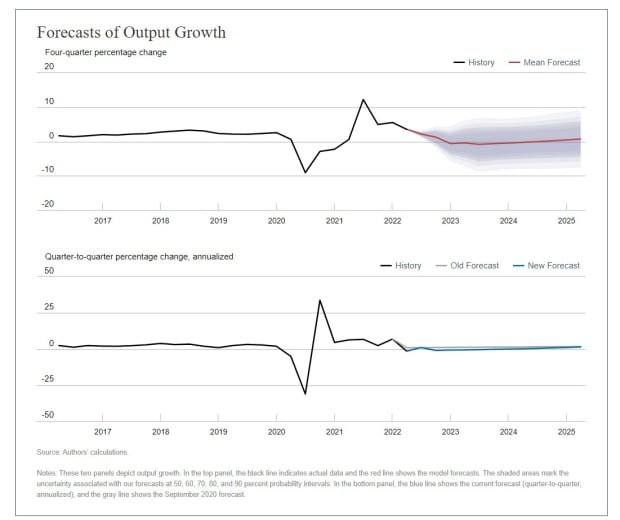

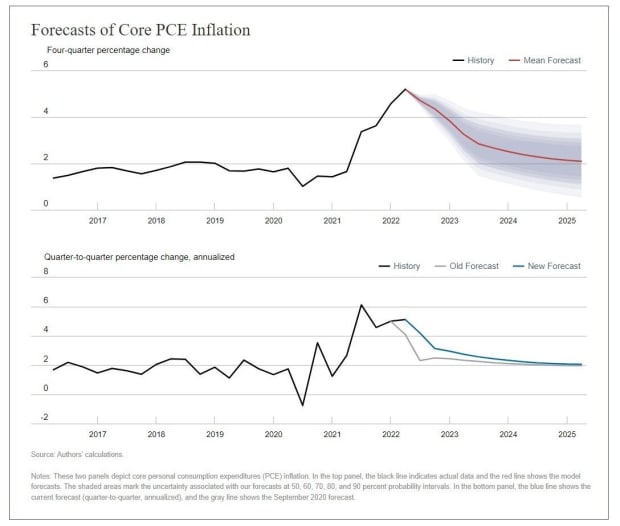

Federal Reserve DSGE Forecasts

Federal Reserve Chairman Jerome Powell went in front of Congress this week and said that a U.S. recession was not his “base case,” despite nearly all economic indicators crashing in the last month.

Here, we take a look at the Fed’s own dynamic stochastic general equilibrium (DSGE) model.

The New York Fed DSGE model has been used to forecast the economy since 2011, and its forecasts have been made public continuously since 2014.

The current version of the New York Fed DSGE model is a closed economy, representative agent, rational expectations model (although we deviate from rational expectations in modeling the impact of recent policy changes, such as average inflation targeting, on the economy). The model is medium scale, in that it involves several aggregate variables such as consumption and investment, but it’s not as detailed as other, larger models.

As you can see below, the model is predicting 2022’s Q4 to Q4 GDP to be negative, as well as the 2023 GDP. That checks with my own estimation and expectation that the U.S. will experience a prolonged but slight recession, while the rest of the world experiences a deeper recession.

In the below chart, I point out the return to the post–Global Financial Crisis (GFC) norm of low growth and low inflation, a norm shared by Japan by the way.

European Anti-Fragmentation Cracks

Only a week after we showed watchers, listeners and readers of “Fed Watch” European Central Bank (ECB) President Christine Lagarde’s frustration at the repeated anti-fragmentation questions, EU heavyweight, Dutch Prime Minister Mark Rutte, comes through like a bull in a china shop.

I read parts of an article from Bloomberg where Rutte claims it’s up to Italy, not the ECB, to contain credit spreads.

What’s the big worry about fragmentation anyway? The European Monetary Union (EMU, aka eurozone) is a monetary union without a fiscal union. The ECB policy must serve different countries with different amounts of indebtedness. This means that ECB policy on interest rates will affect each country within the union differently, and more indebted countries like Italy, Greece and Spain will suffer a greater burden of rising rates.

The worry is that these credit spreads will lead to another European debt crisis 2.0 and perhaps even political fractures as well. Countries could be forced to leave the eurozone or the European Union over this issue.

A Look Back On 100 Episodes

The last part of this episode was spent looking back at some of the predictions and great calls we’ve made. It didn’t go according to my plan, however, and we got lost in the weeds. Overall, we were able to highlight the success of our unique theories put forward by this show in the Bitcoin space:

- A strong dollar

- Bitcoin and USD stablecoin dominance

- The U.S.’s relative decentralization makes the country a better fit for bitcoin

- Bearishness on China and Europe

We also highlight some specific calls that have been spot on, which you’ll have to listen to the episode to hear.

I wanted to highlight these things to show the success of our contrarian views, despite being unpopular among Bitcoiners. This show is an important voice in the Bitcoin scene because we are prodding and poking the narratives to find the truth of the global monetary system.

Charts for this episode can be found here.

That does it for this week. Thanks to the watchers and listeners. If you enjoy this content, please subscribe, review and share!

This is a guest post by Ansel Lindner. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.