How many bitcoin users are there? How should we define a bitcoin user? An analysis for categorizing and tracking user growth compared to other estimates.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Note: This article does not include all the data and analysis. The whole piece can be found here.

Bitcoin User Adoption

One of the strongest cases for bitcoin is its growing network effects. For bitcoin to continue to grow in the future, it needs adoption and demand. That demand comes from either growth in more capital flowing into the network and/or growth in its number of users.

Yet, defining someone who uses the Bitcoin network or is a user of bitcoin the asset is incredibly difficult and can have many definitions depending on whom you ask. This piece aims to aggregate and analyze the various definitions and estimates for bitcoin users, define our preferred view of bitcoin adoption and make our own estimations for current bitcoin users.

How Do You Define A Bitcoin User?

There’s no “right” answer in defining a bitcoin user but we considered the following questions when coming up with our definition:

- Is someone who is storing bitcoin on an exchange considered a user or should we only count those who have some form of self custody?

- What’s the nuance between counting on-chain addresses versus accounts or entities?

- Is there a threshold of bitcoin ownership that we should consider for adoption? Is that threshold denominated in bitcoin, fiat currency or as a share of net wealth?

- Is a user defined as someone who just holds bitcoin or do they need to actively transact on-chain or on Lightning?

- Would a merchant who uses the Lightning Network payment rails because of the cheaper fees but elects to immediately convert funds to fiat currency be a user?

- Does a user need to run a node?

It’s likely best to think about bitcoin user adoption in stages or as different buckets. Some rough categories to think about different user types:

- Casually Interested: User owning any amount of bitcoin or bitcoin-related product. This could be someone with $5 in an old wallet, a share of GBTC or someone who dabbled with buying a small amount of bitcoin once on Coinbase.

- Allocator/Investor: User who purchases bitcoin or bitcoin-related products on a recurring basis. Primarily interested in making financial gain on bitcoin’s potential price appreciation. May or may not self custody or use a custodial solution. Likely has 1-5% allocation of their net worth in bitcoin/bitcoin products.

- Heavy User: User who stores a significant portion of net worth in bitcoin through self custody and/or actively engages in on-chain or Lightning transactions. Someone primarily interested in using a separate form of money and monetary network. Likely has more than 5% allocation of their net worth in bitcoin.

Many of the eye-popping adoption numbers that we see today tend to track these categories together. Maybe that’s the right approach for a high-level view of potential adoption and the first touchpoint, but it doesn’t tell us much about the number of users using bitcoin for its primary purpose: decentralized peer-to-peer cash where users can store and transact value on a separate monetary network. Ideally, we want to track the growth of heavy users to reflect meaningful adoption of bitcoin.

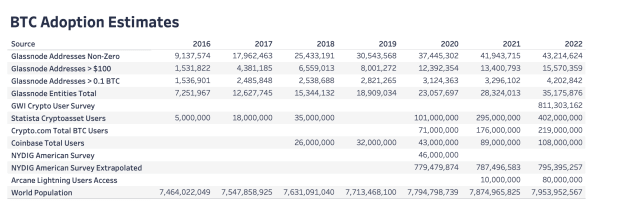

The below table aggregates some of the key bitcoin user estimates that have been published over the last six years to give you an idea of how varying these estimates can be. Looking at casually interested users, numbers from 2022 range from 200 to 800 million users. These are counts from survey samples, data from on-chain analytics and includes exchange users. All of these studies have different definitions and methodologies for calculating adoption, showing how difficult it is to compare estimates out there today.

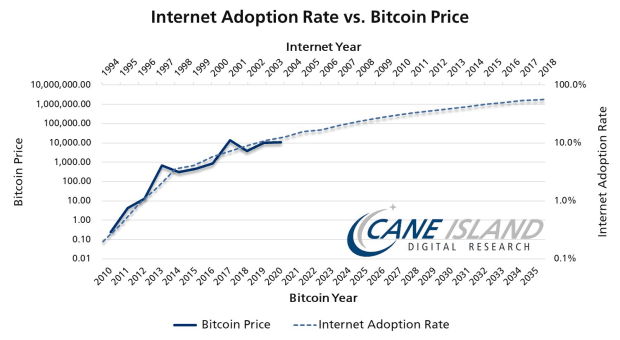

Technology Adoption S-Curve: Internet Versus Bitcoin

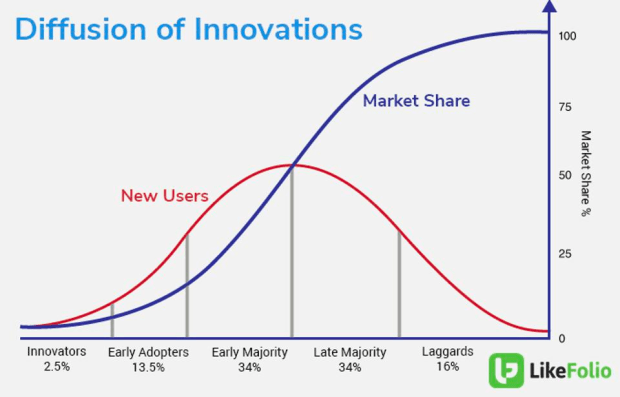

New technologies typically go through an S-curve cycle as they gain market share. Adoption by the population falls into a typical statistical bell curve. An S-curve just reflects the typical adoption path for innovative technologies over time.

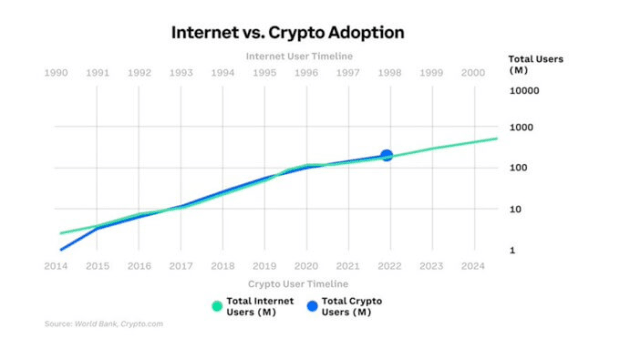

Many of the classic projections for S-curve adoption use a more high-level view of the casually interested users to track bitcoin growth compared to internet adoption. Basically, these estimates track interested users of all types: those who have had any touch points with bitcoin from buying a little bit on an exchange, having a wallet with $5 worth of bitcoin to the bitcoin user storing greater than 50% of their net worth in self custody.

Tracking casually interested users would give people a ballpark estimate of around the same adoption curve as the internet. However, if we’re really interested in tracking meaningful, lasting bitcoin adoption then we would argue that tracking the number of heavy users is a better measure for the current state of bitcoin adoption and emphasizes just how early in Bitcoin’s lifecycle we are. When looking at the more popular analysis comparisons that have previously circulated (included below), they paint a picture that bitcoin adoption is much further along than we calculate it to be.

In 2020, Croseus wrote a thread that analyzes bitcoin adoption in a similar way that we set out to do in this piece. His conclusions show a similar view to our own: Significant bitcoin adoption is much lower than the estimates of 10-15% penetration or roughly 500 million users that are commonly thrown around today. In fact, he suggests that bitcoin adoption by what we would consider “heavy users” is at 0.01% penetration of the global population.

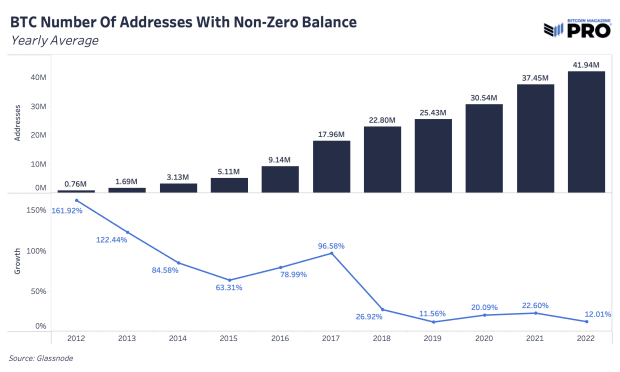

Addresses

The easiest place to start with estimating users is on-chain addresses. Addresses don’t translate to the number of users, but can act as a rough proxy for overall growth. Unique addresses with bitcoin amounts can be growing as new users acquire bitcoin or as current bitcoin holders use many unique addresses to spread out their holdings — a common privacy practice.

We’ve seen an explosion in address growth since 2012 from just under 1 million to nearly 42 million unique addresses today. Let’s say we use an assumption for average addresses per person to be 10 — which is just a rough guess — then the ceiling of bitcoin users who have their own addresses is around 4.2 million.

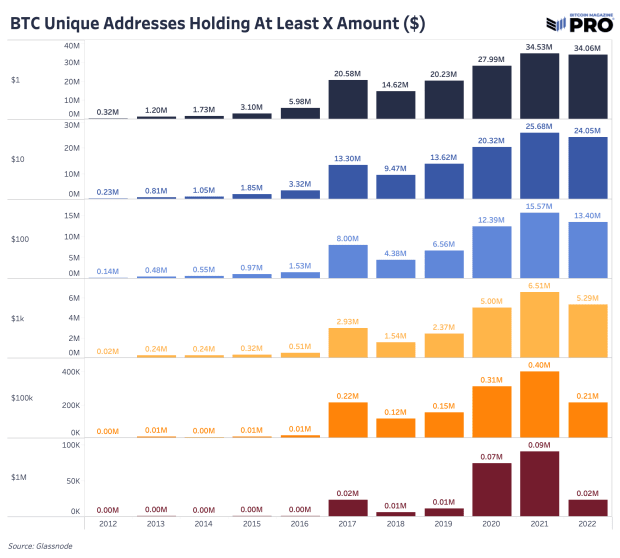

From a USD perspective, there are only 5.3 million addresses holding at least $1,000 worth of bitcoin. Using our rough assumption of 10 addresses per person again then we’re under 1 million users with $1,000 worth of bitcoin. With a global median wealth per adult of $8,360, a bitcoin allocation of $1,000 would make up a significant share of nearly 12%. A relatively small allocation for some, but considering bitcoin is global and has higher adoption rates in less wealthy countries, the benchmark seems fitting.

Using our definition of “heavy user” to calculate, if we use addresses with a certain threshold of BTC or USD and make some rough assumptions around addresses per person along with not counting exchange users or addresses holding bitcoin on the behalf of others, then this approach estimates only 593,000 bitcoin users.

We go into more detail about other ways to analyze bitcoin users in an article on Substack. No matter which way you cut the data, there is not a large amount of the worldwide population who would be considered heavy users who self-custody a significant threshold of bitcoin.

Conclusion

The analysis in this article is meant to highlight how difficult it is to define and track bitcoin user growth in a reliable way.

We are highlighting a lower penetration of adoption not to dissuade readers from the growth of bitcoin’s network effects so far, but rather to highlight the substantial opportunity of its potential growth in the future.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

Relevant Articles:

- BM Pro Market Dashboard Release!

- Bitcoin Rips To $21,000, Shorts Demolished In Biggest Squeeze Since 2021

- Bitcoin Sellers Exhausted, Accumulators HODL The Line

- Time-Based Capitulation: Bitcoin Volatility Hits Historic Lows Amid Market Apathy

- 2022 Year In Review